Contagion spillovers between sovereign and nancial European sector from a CoV aR approach 23 de maio de 2018

Visto 44

veces

Contagion spillovers between sovereign and nancial European sector from a CoV aR approach

ECOBAS (Economics and Business Administration for Society) é un Centro de Investigación Interuniversitario integrado por persoal investigador e docente das tres universidades galegas, e especializado no estudo da sustentabilidade económica, ambiental e social. Integrado por un equipo de preto dun centenar dos mellores académicos e académicas das tres universidades galegas no ámbito das ciencias sociais, ECOBAS traballa para tratar de dar resposta ós grandes retos e desafíos da sociedade a través da investigación, a docencia, a innovación, e a transferencia de coñecemento.

i18n.one.Series:

Mediateca Ecobas

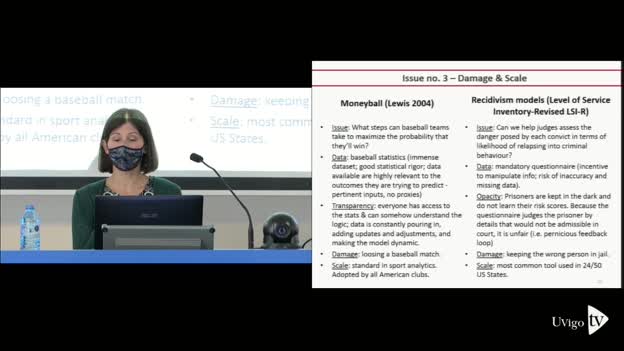

Javier Ojea

Foundations of Economic Analysis II, Universidad Complutense de Madrid

Vídeos da mesma serie

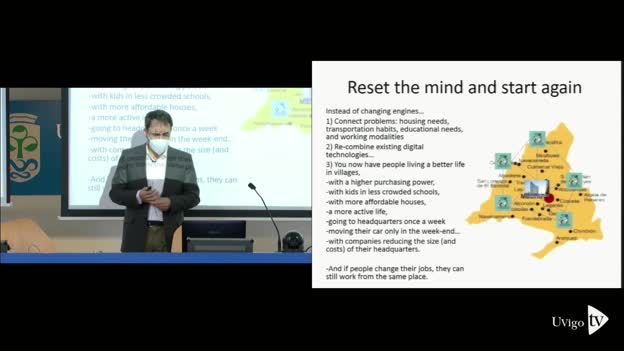

The impact of climate transition risks on financial stability. A systemic risk approach

Conference

11 de mar. de 2022

The impact of group identity on social responsibility and welfare in experimental markets

Conference

21 de xan. de 2022

Competencia e desigualdade de xénero: unha análise integral de efectos e mecanismos

Conferencia

5 de nov. de 2021

Unthinking "Capital": a teratologic approach to concept formation

Mediateca Ecobas (Economics and Business Administration for Society)

27 de out. de 2021

Prospering without growth. Science, Technology and innovation in a post-growth era

Conference

5 de out. de 2021

El reto de construír un contrato social justo y sostenible

Antón Costas Catedrático de Política Económica e presidente do Consello Económico e Social de España, reivindica o contrato social para garantir un funcionamento sostible da economía de mercado e para previr a barbarie política, ademais de incidir na importancia de sostenibilidade social e na necesidade de recuperar a prosperidade compartida.

17 de set. de 2021

Xestión óptima de xerarquías en evolución

Mediateca Ecobas (Economics and Business Administration for Society)

9 de set. de 2021

Brave Boys and Play-it-Safe Girls: Gender Differences in Willingness to Guess in a Large Scale Natural Field Experiment

Seminarios Ecobas 2020 | Nagore Iriberri Professor at the Department of Foundations of Economic Analysis I at the University of the Basque Country UPV/EHU

26 de feb. de 2020

Tamén che interesan

COPA-DATA: Benvido ao 2030: "Plug & Produce", o potencial da fabricación modular

Conferencia

18 de nov. de 2022

Alumnos Uvigo opinan: Grao en Linguas Estranxeiras

Universidade de Vigo: aquí todo é posible

27 de abr. de 2016

Redución das emisións de CO2 na automatización da industria da automoción

Conferencia

18 de nov. de 2022

Automatización de procesos produtivos con fabricación aditiva. Estudo de caso: tecnoloxía HP Multi Jet Fusion en odontoloxía

Conferencia

18 de nov. de 2022